Introduction: The hangover after the gold rush

For more than a decade, Medicare Advantage (MA) looked like one of the most reliable engines in American healthcare. Enrolment increased year after year. Plans expanded benefits. Provider groups built their value-based strategies around rising MA membership, robust risk adjustment payments, and predictable quality bonus flows. Entire care delivery models were constructed on the assumption that MA penetration would continue to grow and risk adjustment would provide steady uplift.

That era is ending. And it’s showing up in 2026 benefit design and market behavior: plan offerings are down year over year, more beneficiaries are facing plan terminations, and many plans are trimming certain supplemental benefits to protect margins.

As experts monitoring this shifting landscape, we see the market confronting a new reality shaped by three converging forces:

- The full implementation of the CMS-HCC V28 risk adjustment model, which fundamentally alters how patient complexity is measured and paid for.

- Slowing or flattening MA enrollment, after more than a decade of uninterrupted expansion.

- Margin compression across MA plans, driven by rising costs, regulatory pressure, and quality measurement volatility.

These shifts represent more than incremental policy changes. Together, they reshape the core economics of care delivery, affecting how providers document disease severity, structure clinical encounters, deploy staffing, and calibrate their financial expectations. The playbook that worked in 2019, 2020, or even 2023 will not work in 2026.

Surviving this new environment requires moving beyond old assumptions rooted in membership growth and broad-based coding. This article examines the forces reshaping the 2026 landscape and outlines the economic strategies that will define the next phase of value-based performance.

The pincer move: The two forces compressing 2026 margins

The most important dynamic in 2026 is what many analysts refer to as a pincer move, two simultaneous pressures that squeeze the economics of MA from opposite sides.

Claw one: The impact of full V28 implementation

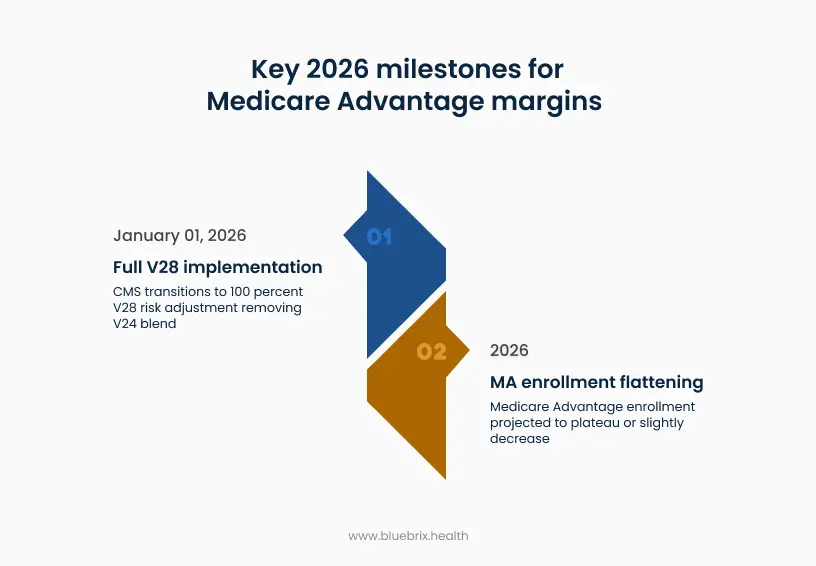

The Centers for Medicare & Medicaid Services (CMS) introduced the updated CMS-HCC model (V28) in 2023 and began phasing it in during 2024 and 2025. In those years, CMS blended the new V28 risk scores with the older V24 model to soften the transition. But as of January 1, 2026, CMS has eliminated the blend entirely. Risk scores now reflect 100% V28, with no buffer from the prior model.

This matters because V28:

- Removes 2,294 ICD-10-CM codes previously used in risk adjustment, particularly unspecified and low-severity diagnoses.

- Reclassifies numerous condition groups to emphasize severity, specificity, and clinical relevance, not just presence of disease.

- Uses updated clinical cost data and ICD-10 classifications that more tightly link diagnosis coding to predicted expenditures.

The financial implication is stark. This shift could translate to an estimated 3-7% reduction in overall RAF scores for a typical MA plan if documentation practices are not fundamentally altered, impacting tens of millions in annual revenue.

The economics shift from “more codes” to “defensible severity.”

A patient documented as “Diabetes” (unspecified severity) may have produced meaningful RAF weight under the old mapping environment. Under V28, that same chart often generates less risk score unless the note supports complications/severity (e.g., “diabetes with chronic complications” plus evidence).

This is not a coding problem. It is an economic shift. Under V28, revenue depends on the accuracy and specificity of clinical documentation, not on the volume of codes captured.

Claw two: The slowdown in MA growth

For years, MA growth masked operational inefficiencies. Organizations could tolerate uneven performance because new membership generated new revenue. That cushion is gone.

Analyses in late 2025 projected that MA enrollment would flatten or modestly decrease (from 34.9M in 2025 to 34.0M in 2026) in 2026. Multiple factors contribute:

- Increased cost pressures leading plans to reduce supplemental benefits.

- Greater scrutiny from members about plan value and provider access.

- Competition between Original Medicare + Medigap and MA plan offerings.

- Market saturation in regions with already high MA penetration.

This shift changes the fundamental calculus of the business model. If membership is no longer growing, organizations must profitably manage the populations they already have and improve per-member economics rather than scaling through volume. The loss of growth-driven subsidies means operational precision now drives financial stability.

Why better coding is a trap in 2026

One common industry response to V28 is to intensify coding activities; hire more coders, expand auditing workflows, or introduce coding prompts. While these efforts can help with organizing documentation, they cannot overcome the structural realities of V28.

The core issue is: V28 financially rewards accurate, severity-aligned documentation; not more documentation.

Under V24, capturing additional diagnoses often produced a meaningful increase in revenue. But V28 is designed to eliminate the benefits of “coding multiplier effects” that do not reflect true clinical burden. CMS has repeatedly stated that the agency intends to reinforce clinical truth, not administrative coding.

Audit risk has increased

Even amid ongoing litigation over the 2023 RADV rule (which a court vacated and CMS appealed), CMS’s audit posture is clearly tightening, including a major expansion strategy to audit all eligible MA contracts in newly initiated audits and accelerate completion of backlogged payment years. CMS is targeting:

- Unsupported severity codes

- Diagnoses without evidence of MEAT (Monitor, Evaluate, Assess, Treat)

- Administrative coding patterns that do not match visit documentation

- Overreliance on retrospective chart reviews

Strategies based on broad code capture can generate high audit exposure with limited financial return.

Severity requires documentation, not coding

A diagnosis like “chronic kidney disease” is insufficient on its own. Under V28:

- CKD Stage 3 vs. Stage 4 reflect different predicted costs.

- Diabetes “with chronic complications” requires demonstration of those complications.

- Heart failure must distinguish between preserved and reduced ejection fraction.

Coding alone cannot create this specificity, the clinical note must demonstrate it. Organizations that treat V28 as a coding exercise are misaligned with both CMS policy and 2026 economic incentives.

Rethinking care delivery economics: The unit economics of a visit

The single biggest shift in 2026 is not about coding. It is about how care delivery itself must operate. V28 changes the economic assumptions beneath every clinical encounter.

Under V24, many provider organizations viewed visit volume and diagnosis capture as the primary drivers of risk adjustment performance. But in a post-V28 world, the economic question shifts from: “How many diagnoses can we capture?” to “How precisely can we document the patient’s actual disease severity?”

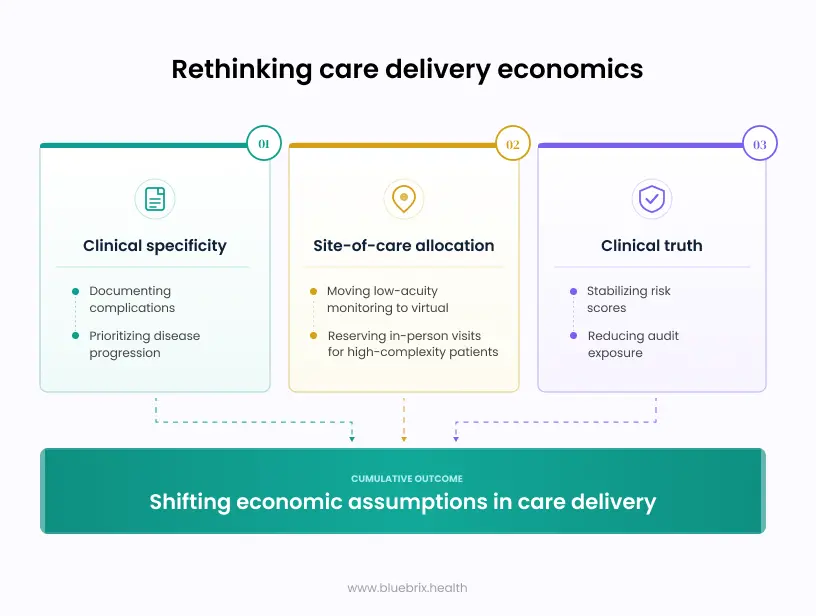

This impacts care delivery in three fundamental ways.

1. Clinical specificity is now a revenue strategy

One clinically accurate, well-supported severe diagnosis has more impact than five unspecified ones. This means:

- Visit time should prioritize understanding disease progression.

- Providers must document complications with clarity, not generalities.

- Teams must enable physicians to record the full clinical picture without increasing administrative burden.

Economic value now flows from depth, not breadth.

2. Clinical truth reduces risk and improves revenue predictability

CMS designed V28 to reflect true patient burden. When documentation matches clinical reality:

- Audit exposure drops dramatically.

- Risk scores stabilize.

- Shared-savings calculations become more predictable.

- Per-member financial forecasting becomes more accurate.

The economic upside is not from higher scores, it is from more defensible scores.

3. Site-of-care allocation becomes a major cost lever

Because margins tighten when unspecified conditions fail to generate RAF weight, organizations must optimize where care happens. This means moving low-acuity monitoring to virtual channels and reserving in-person visits for high-complexity patients. This is not about cost-cutting. It is about economically aligning visit type with clinical need.

The three pillars of the 2026 care delivery model

To navigate the new environment, successful organizations are building around three interlocking pillars that reflect both CMS policy direction and economic constraints.

Pillar one: Prospective precision

The traditional model (retrospective chart review, followed by coding cleanup) is no longer efficient. Instead, organizations must:

- Identify suspected diagnoses based on longitudinal data.

- Pre-load charts with relevant clinical indicators before the visit.

- Ensure that complex patients receive longer appointment slots.

This shifts documentation efforts into a prospective, clinically aligned model. The goal is to place the provider in a position to validate or clarify severity, not to discover it retroactively.

Pillar two: Concurrent documentation support

The clinical encounter is now the center of economic gravity. Organizations that remove documentation friction from the provider see the greatest gains. This includes real-time transcription that captures nuance and concurrent AI structuring that aligns notes with clinical reasoning.

Concurrent documentation ensures that the provider’s clinical thinking translates into compliant, defensible notes before the note is signed, not weeks later.

Pillar three: Audit-proofing as a core strategy

In a post-V28 world, audit risk is no longer a compliance footnote, it is an economic driver.

Organizations must invest in:

- Clinical documentation integrity (CDI) teams focused on severity, not volume.

- Review processes that verify MEAT requirements are met.

- Predictive analytics to flag unsupported diagnoses before submission.

- Longitudinal care plans that connect diagnoses to interventions, labs, or follow-up.

Audit-proofing is now a front-end function, not a back-end correction.

What this means for contracting and financial strategy

The shift in care delivery economics reverberates across contracting strategies, plan-provider relationships, and value-based care performance.

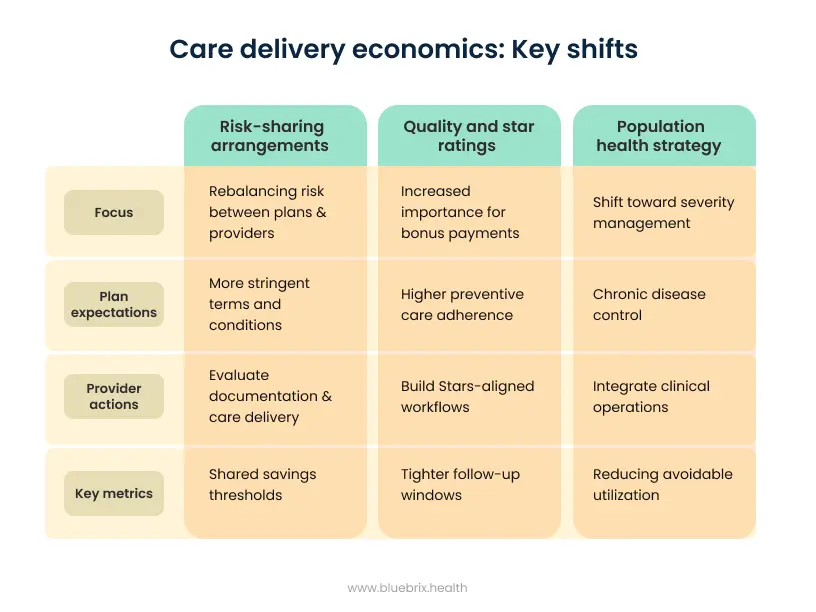

Risk-sharing arrangements will rebalance

As plans confront higher costs, lower rebate cushions, and greater pressure on benefits, many will revisit:

- shared savings thresholds

- medical loss ratio expectations

- utilization guardrails

- stop-loss corridors

- benchmark assumptions

Providers must be prepared for more stringent terms and must evaluate whether their own documentation and care delivery models can support those terms under V28.

Quality and star ratings will matter more

CMS is actively reworking Star Ratings for contract year 2027, simplifying measures and focusing on outcomes. Because Stars drive bonus payments that support benefits, volatility here directly affects provider economics. Plans under pressure from Stars recalibration will demand:

- Higher preventive care adherence

- Tighter follow-up windows

- Consistent documentation of chronic conditions

- Improved care coordination metrics

Providers who build Stars-aligned workflows into their care delivery model will gain contracting leverage.

Population health strategy must shift toward severity management

Risk adjustment and Stars are increasingly aligned around:

- Chronic disease control

- Reducing avoidable utilization

- Ensuring continuity of care

- Improving medication adherence

- Identifying rising-risk patients early

Organizations must integrate clinical operations with population health strategy, not treat them as separate domains.

Ready to secure your 2026 economics?

The shift to V28 requires more than just awareness—it requires an actionable roadmap. Don’t let margin compression catch your organization off guard.

Let’s connect for a complimentary executive briefing and identify your most critical gaps before the quarter ends.

Contact us